Staring at a blank spreadsheet trying to calculate your freelance financial projections can feel like trying to read a foreign language. But if you want to survive as a solo operator, you have to know your numbers — and the good news is the math is simpler than you think.

I learned this the hard way. For my first two years freelancing, I ran my business by checking my bank balance. Positive number? Keep going. That worked fine until a surprise $4,000 tax bill nearly wiped me out in January. That financial blindspot is exactly why we built Smart Remote Gigs — to give independent contractors the exact math frameworks they need to protect their income, without the MBA corporate fluff. I didn’t need a Wall Street financial model to avoid that tax bomb. I needed three numbers on a napkin. That’s what this guide gives you.

The 3-Number Freelance Forecast

- Minimum Viable Income (MVI) — The exact baseline dollar amount you need to survive.

- The 30% Tax Rule — The non-negotiable slice of every invoice you must hide from yourself.

- The Profit Target — The stretch goal you need to hit to actually build wealth, not just pay rent.

Why You Don’t Need an Accounting Degree to Forecast

Corporate financial projections exist to answer one question: “Will investors get their money back?” You don’t have investors. You have a skills-based service business with low overhead, variable income, and no shareholders to answer to.

That means the entire apparatus of traditional forecasting — EBITDA calculations, depreciation schedules, break-even analysis — is irrelevant to your situation. What you actually need is a dead-simple cash flow model that tells you three things: how much you must earn, how much goes to taxes, and how much you need to grow.

The IRS Statistics of Income Division consistently shows that the majority of self-employed sole proprietors operate with fewer than five expense line items. Your financial model should reflect that reality, not pretend you’re running a manufacturing company.

Warning: Don’t get stuck building 5-year models. As a freelancer, your most accurate and actionable projection is the next 90 days. Anything beyond that is informed guesswork. Plan the quarter, execute the quarter, then reforecast. That’s the entire system.

Step 1: Calculate Your Minimum Viable Income (MVI)

Your MVI is the single most important number in your freelance business. Everything else — your pricing, your client load, your marketing intensity — is calibrated against it.

Here’s how to calculate it. Open a blank page and list every fixed monthly expense in your life:

- Rent or mortgage

- Groceries and household basics

- Health insurance (this one stings as a solo operator — don’t underestimate it)

- Phone and internet

- Software subscriptions (your business tools)

- Transportation

- Minimum debt payments

- Any other non-negotiable recurring costs

Add them up. That raw number is your personal MVI — what you need to not go backwards.

Now add your business overhead: software licenses, coworking space if applicable, professional development, equipment depreciation. For most freelancers, this adds $200–$600/month to the number.

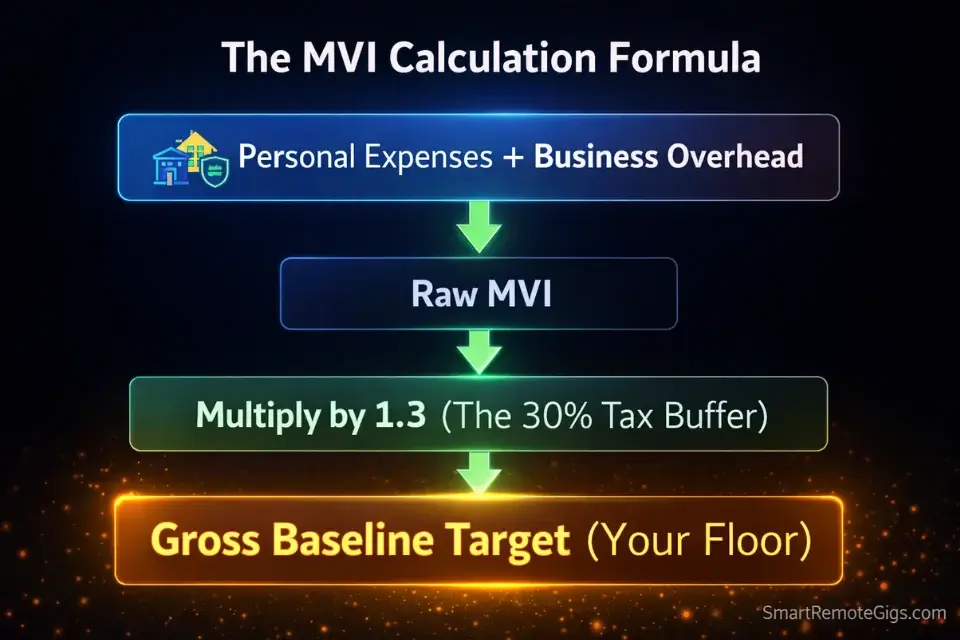

Pro Tip: Once you have your raw monthly MVI, multiply it by 1.3. That 30% buffer accounts for self-employment taxes. The result is your actual baseline gross revenue target — the minimum your business must generate before you keep a single dollar. This number should be the first thing in every financial plan you build.

For example: $5,000 raw MVI × 1.3 = $6,500/month gross baseline. That’s your floor. Not your goal — your floor.

Your MVI doesn’t sit in isolation. It’s the foundation of your entire operating plan, which is why it’s the first financial block in the freelance business plan framework. If you haven’t built that plan yet, your MVI is the number you start with.

Step 2: The “Self-Employment Tax” Reality Check

This is the section most freelance guides skip, and it’s the section that causes the most financial pain.

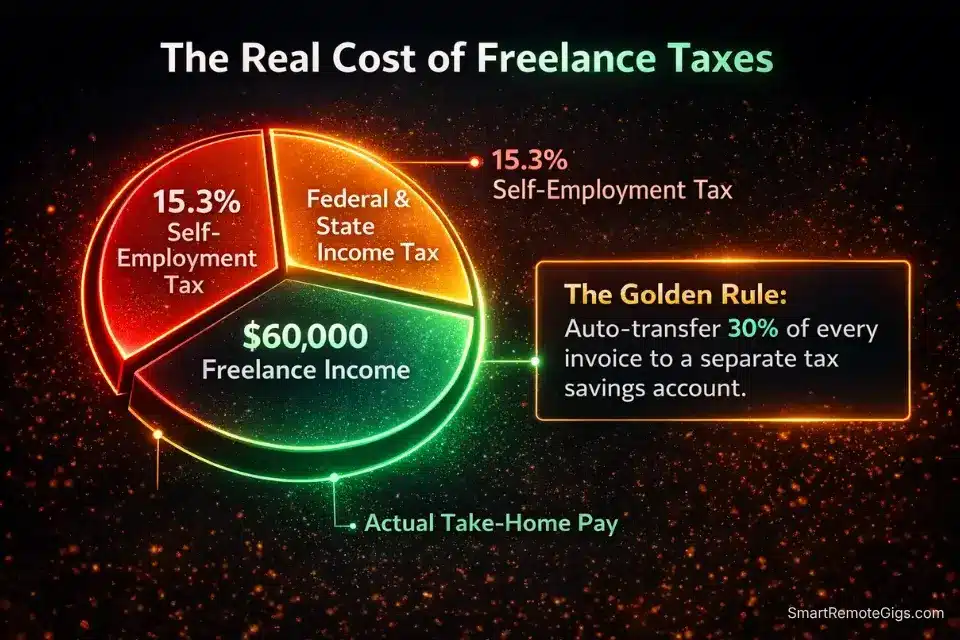

When you work as an employee, your employer pays half of your Social Security and Medicare taxes on your behalf. When you’re self-employed, you pay both halves. That’s the 15.3% self-employment tax — 12.4% for Social Security and 2.9% for Medicare — applied to your net self-employment income before federal and state income tax even enters the picture.

Here’s what that looks like on a $60,000/year freelance income:

- Gross revenue: $60,000

- SE tax (15.3%): $9,180

- Federal income tax (22% bracket after deductions): ~$7,500

- State income tax (varies — assume 5%): ~$3,000

- Total tax burden: ~$19,680

- Take-home: ~$40,320

That’s a 33% effective tax rate before you’ve bought a single business expense. The 30% rule isn’t conservative — for many freelancers in mid-range income brackets, it’s barely adequate.

The practical action: open a separate savings account today and automatically transfer 30% of every invoice payment into it the moment it lands. Treat it as money that doesn’t exist. This one habit eliminates the “surprise tax bill” experience entirely.

Your legal structure also affects this math in meaningful ways. An S-Corp election through a Single-Member LLC can reduce your SE tax exposure once you cross certain income thresholds — the freelance business structure guide breaks down exactly when that transition makes financial sense.

Step 3: Projecting Revenue (Hourly vs. Retainer Models)

Not all freelance income is created equal. How you price your services has a dramatic effect on how predictable and forecastable your revenue actually is.

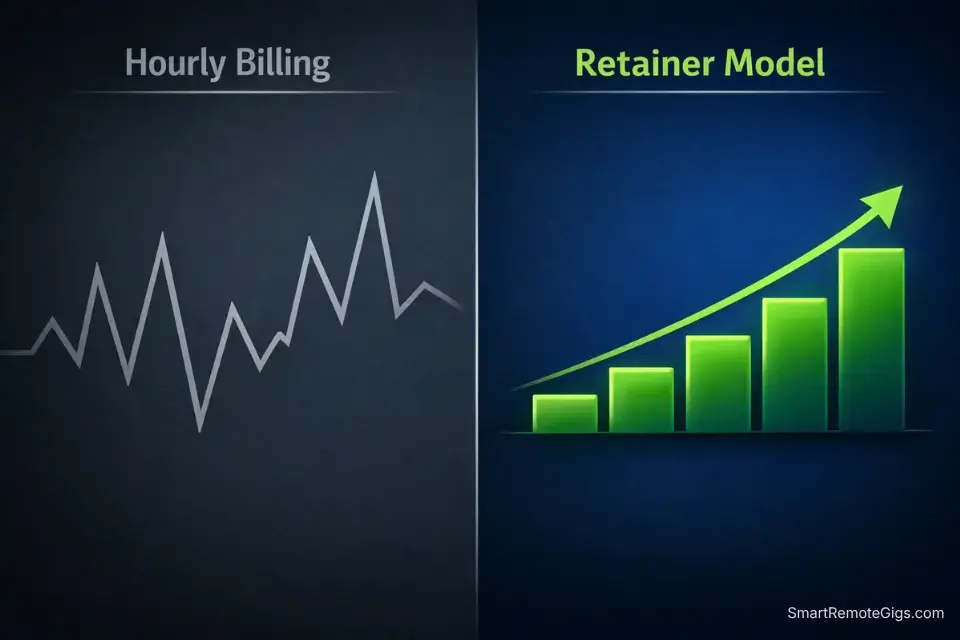

Hourly billing is highly volatile. Your income depends on how many hours you work, how many clients are active, and whether anyone goes quiet this month. It’s hard to project because every variable changes weekly.

Retainer billing is the closest a freelancer gets to a salary. A client pays a fixed monthly fee for a defined scope of work. Your revenue for that client is locked in for the contract term. Stack three to four retainer clients and your income becomes genuinely forecastable 60–90 days out.

Here’s how the two models compare at the same annual revenue target:

Factor | Hourly Billing | Retainer Model |

|---|---|---|

Income Predictability | Low — varies month to month | High — fixed monthly amount |

Revenue Ceiling | Capped by billable hours available | Expandable by adding clients |

Forecasting Difficulty | High — too many variables | Low — math is simple multiplication |

Client Relationship | Transactional, project-by-project | Ongoing, higher trust and LTV |

Cash Flow Gaps | Common — feast or famine cycles | Rare — income arrives on schedule |

Best For | Early-stage, testing the market | Established freelancers with proven offer |

Practical projection math for each model:

Hourly: (Average weekly hours × hourly rate × 48 working weeks) × 0.7 (tax adjustment) = estimated annual take-home

Retainer: (Monthly retainer value × number of clients × 12) × 0.7 = estimated annual take-home

The retainer version is simpler to calculate, simpler to manage, and simpler to grow. If you’re currently billing hourly, converting even one client to a monthly retainer will immediately improve the quality of your financial projections.

Automating Your Numbers with the Right Software

Manual spreadsheets work until they don’t. The moment you have more than two active clients and a handful of expense categories, a spreadsheet becomes a part-time job in itself — one that doesn’t bill by the hour.

Accounting software solves three specific problems for freelancers: it categorizes expenses automatically for tax deductions, it generates real-time P&L statements so you always know where you stand, and it calculates your quarterly estimated tax payments so you’re never caught off guard.

I made the switch from spreadsheets to dedicated software when I hit $40k in annual revenue. I wish I’d done it at $20k. The time savings alone justified the cost within the first month, and I recovered $3,200 in deductions my spreadsheet had missed in the prior year.

The honest downside: QuickBooks has a habit of raising its subscription prices with little warning, and the full interface can feel genuinely overwhelming if all you want to do is send an invoice and set aside your tax slice. If you’re under $30k/year, Wave — which is free — handles the basics without the bloat. QuickBooks earns its price once your expense categories, deduction tracking, and quarterly estimates become complex enough to actually need it.

For a broader look at which tools are worth paying for at each stage of your freelance operation, the top tools for freelancers guide ranks the full stack with honest pricing breakdowns.

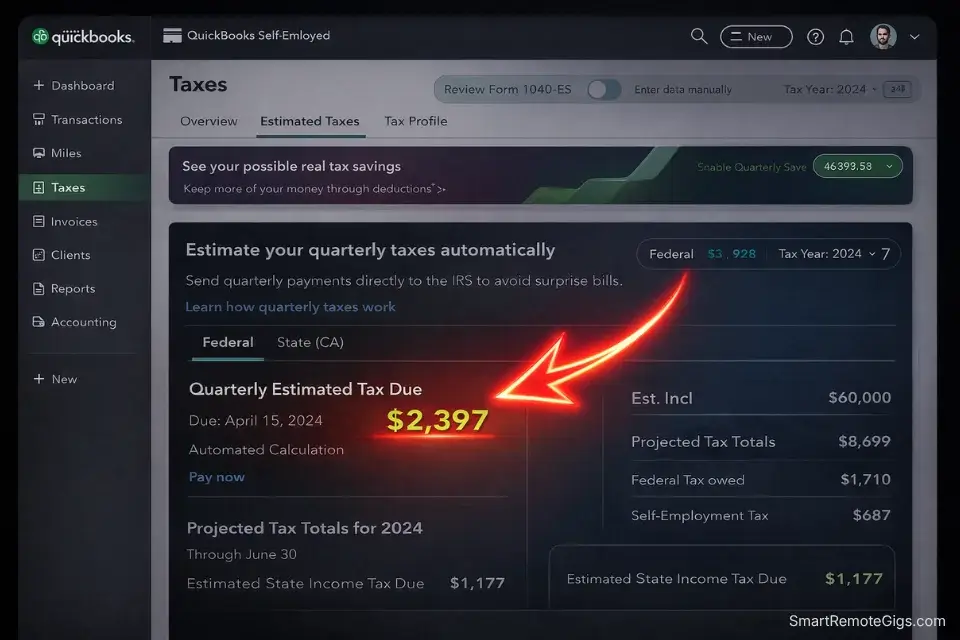

QuickBooks

Best for: Freelancers who have crossed $30k/year in revenue and need automated expense categorization, quarterly tax estimates, and a real P&L without hiring a bookkeeper.

Frequently Asked Questions

How do I calculate financial projections as a freelancer?

Start with your monthly personal expenses, add your business overhead, then multiply the total by 1.3 to account for taxes. That gives you your monthly gross revenue floor. Multiply by 12 for your annual baseline.

From there, divide by your average project or retainer price to get the minimum number of clients you need to break even. Everything above that number is profit. The math is genuinely that simple — the difficulty is being honest about your actual expenses rather than rounding down to feel better.

What is a good profit margin for a freelance business?

Because solo freelancers operate with minimal overhead — no office, no payroll, no inventory — a healthy net profit margin sits between 60% and 80% before personal taxes. That figure drops significantly if you’re not tracking deductible expenses properly.

Home office costs, software, professional development, internet, and equipment all reduce your taxable income. If your margin is below 50%, you either have a pricing problem, an untracked expense problem, or both.

Do I need software to track freelance finances?

You can start with a simple template in the early stages — our 1-page Notion business plan template includes a basic financial tracking block that works fine under $30k/year. Once you cross that threshold, transitioning to dedicated accounting software becomes genuinely important.

Managing quarterly estimated tax payments manually gets expensive when you miscalculate, and deduction tracking in a spreadsheet is easy to let slip. The software pays for itself in recovered deductions within the first tax season.

The Verdict & Final Action Step

Simple math executed consistently always beats a complex spreadsheet you never update.

You don’t need a financial model. You need your MVI, your tax buffer, and your revenue target — three numbers you can write on an index card. Once those are locked in, every business decision becomes easier: whether to raise your rates, how many clients you need to feel stable, when it’s safe to take a week off.

The freelancers who feel financially anxious almost always share one trait: they don’t know their MVI. The ones who feel calm and in control almost always know it to the dollar.

Calculate yours today. It takes ten minutes and eliminates more stress than any amount of extra hustle will.

Verdict: Knowing your MVI is the single highest-leverage financial move a freelancer can make. It converts vague income anxiety into a specific, solvable math problem. Set your 30% tax transfer on autopilot, know your gross revenue floor, and spend the rest of your energy on selling — not on staring at spreadsheets. The numbers are simpler than you’ve been told.

🎁 Free Digital Asset: 1-Page Business Plan

Download the 1-page business plan template to plug in your MVI and revenue targets right now.

Complete 2026 Methodology: Creating an Agile Freelance Business Plan

The three numbers in this guide — MVI, tax buffer, profit target — aren’t standalone calculations. They slot directly into your 1-page operating plan as the financial foundation everything else is built on.

Here at Smart Remote Gigs, this agile, math-first approach is the exact methodology we teach to keep remote freelancers out of the feast-or-famine cycle. You don’t need to be an accountant; you just need to follow the formula. Know your floor. Protect your tax slice. Chase your target. That’s the whole financial system.