Choosing the right freelance business structure shouldn’t feel like navigating a legal minefield. But if you pick the wrong entity at the wrong time, you could expose your personal savings to client lawsuits — or waste hundreds of dollars in state filing fees before you’ve earned your first dollar.

I made the second mistake. I panicked before launching and paid $800 to form an LLC before I had signed a single client. It was a massive waste of startup capital that solved a problem I didn’t have yet. I learned the hard way that you can validate your business for free first, then upgrade your legal protection when the stakes actually matter.

Preventing other solo operators from making these expensive, panic-driven legal mistakes is exactly why we built Smart Remote Gigs. We exist to cut through the jargon and give you clear, BS-free operational frameworks. This guide tells you exactly when that moment to upgrade is.

Sole Proprietor vs. LLC at a Glance

- Sole Proprietor: $0 to start. Your default legal status the moment you start working for yourself. Zero separation between personal and business assets. Best for absolute beginners testing the waters.

- Single-Member LLC: Costs $50–$500+ depending on your state. Creates a legal “corporate shield” that separates your personal savings and property from any business liability. Best for established freelancers with consistent income and real assets to protect.

The Baseline: Operating as a Sole Proprietor in 2026

Here’s something most freelancers don’t realize: you are already a Sole Proprietor. The moment you perform paid work for a client under your own name, US law automatically classifies you as one. There is no form to file, no fee to pay, and no government office to notify.

Your business income gets reported directly on your personal tax return via Schedule C. Your business expenses are deducted on the same form. From the IRS’s perspective, you and your business are a single entity — which is both the simplicity and the danger of this structure.

The IRS’s official Sole Proprietor resource page confirms that sole proprietorships are the most common business structure in the US for exactly this reason: zero friction to start, minimal ongoing administration, and straightforward tax treatment.

Warning: Operating as a Sole Prop means you and the business are legally identical. If a client sues you — over a missed deadline, a deliverable dispute, or a data handling issue — they aren’t suing your business. They’re suing you. Your personal bank account, your car, your savings, and depending on your state, potentially your home, are all on the table. This isn’t a hypothetical risk. It’s the default legal reality of Sole Proprietorship.

The Upgrade: Forming a Single-Member LLC

A Single-Member LLC does one primary job: it builds a legal wall between your business and your personal life.

That wall is called the corporate shield or limited liability protection. When your business operates as an LLC and a client files a lawsuit, they can pursue your business assets — your business bank account, your equipment, your receivables. They cannot, in most circumstances, touch your personal savings, your home, or your personal accounts. That separation is the entire value proposition of the LLC for a solo freelancer.

What an LLC does not do — and this is where most freelancers get confused — is automatically reduce your taxes.

A standard Single-Member LLC is classified by the IRS as a “disregarded entity.” That means for federal tax purposes, you’re still treated exactly like a Sole Proprietor. Your income still flows to Schedule C. You still pay the full 15.3% self-employment tax. The LLC filing itself changes your legal protection, not your tax bill.

The tax advantage only arrives if you make a separate election to be taxed as an S-Corporation — a move that makes sense above roughly $60,000–$80,000 in annual net profit, and only after you’ve consulted with a CPA about your specific situation. Below that threshold, the administrative cost of running payroll (required for S-Corp status) typically exceeds the tax savings.

LLC vs. Sole Proprietor: The 6 Crucial Differences

Factor | Sole Proprietor | Single-Member LLC |

|---|---|---|

Cost to Form | $0 — automatic default status | $50–$500+ in state filing fees (varies significantly by state) |

Personal Asset Protection | None — personal and business assets are legally identical | Strong — corporate shield separates personal from business liability |

Administrative Burden | Minimal — just file Schedule C annually | Moderate — annual state reports, registered agent fees, separate banking required |

Tax Treatment | Pass-through to personal return via Schedule C | Same pass-through by default; S-Corp election available above ~$60k net profit |

Credibility Signal | Lower — some enterprise clients prefer contracting with LLCs | Higher — “LLC” in your business name signals legitimacy to larger clients |

Banking Requirement | Separate account recommended but not legally required | Separate business account mandatory — commingling funds can void the corporate shield |

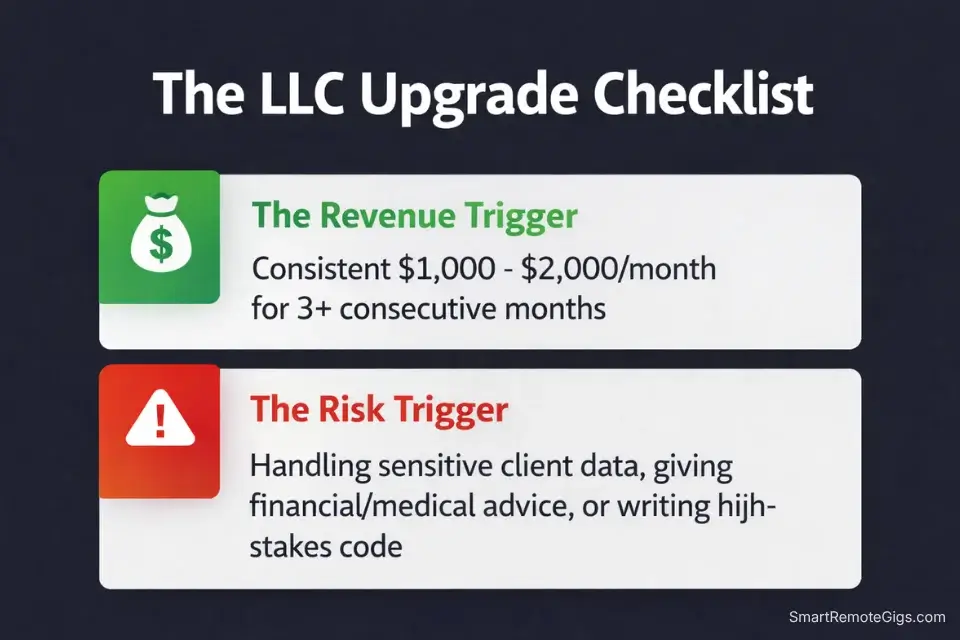

The “Triggers”: Exactly When to Switch to an LLC

This is the question I wish someone had answered for me clearly before I wasted $800. Here are the two specific triggers that signal it’s time to upgrade.

The Revenue Trigger

Once you’re consistently generating $1,000–$2,000/month for three or more consecutive months, your LLC filing fees become a rounding error relative to what you’re protecting. At that revenue level, you likely have a business bank account with real money in it, active contracts with real obligations, and enough momentum that a single client dispute could do real damage if you’re personally exposed.

Consistent is the key word. One good month doesn’t justify the overhead. Three consecutive months of similar revenue does.

The Risk Trigger

Some freelance niches carry inherently higher liability than others, regardless of income level. If your work involves any of the following, form an LLC sooner rather than later:

- Handling sensitive client data (HIPAA-adjacent work, financial records, PII)

- Medical or health writing where advice could influence patient decisions

- Financial consulting or anything adjacent to investment guidance

- Legal support work or paralegal services

- Software development where bugs could cause client financial loss

In high-liability niches, even one early-career contract justifies the filing cost. The asymmetry between a $150 state filing fee and a five-figure lawsuit is not a close call.

Pro Tip: Not all states are created equal on LLC costs. Delaware and Wyoming are popular for low fees and flexible statutes. California charges an $800 minimum annual franchise tax on LLCs regardless of revenue — meaning a California freelancer earning $1,200/month is paying $800/year just to maintain the entity. Always look up your specific state’s annual recurring fees before filing, not just the one-time formation cost. The National Conference of State Legislatures maintains updated state-by-state business formation resources.

How Your Structure Impacts Your Finances and Taxes

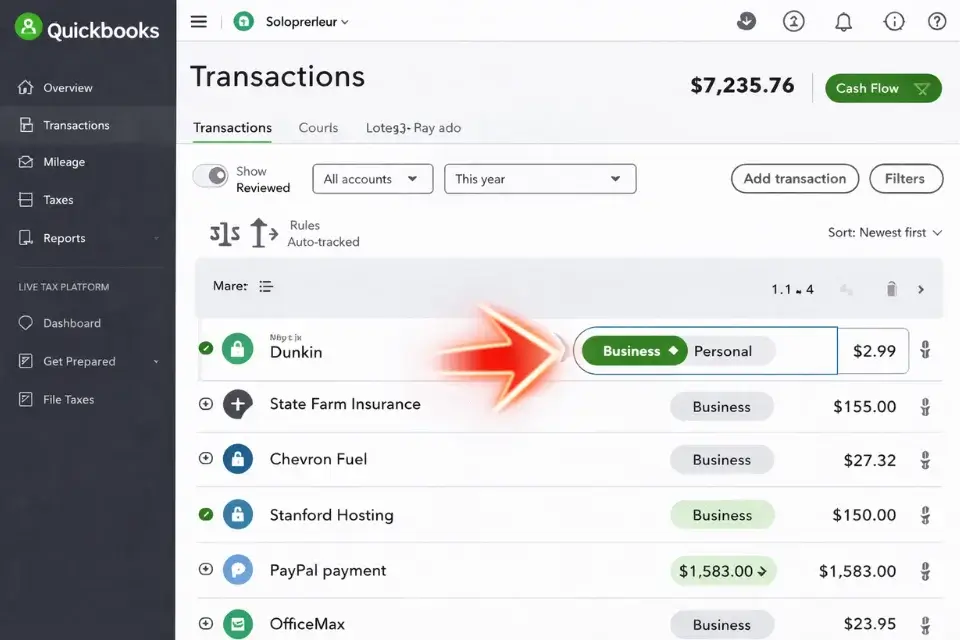

Regardless of which structure you choose today, there is one action that applies to both: open a dedicated business bank account immediately and never mix personal and business funds.

For Sole Proprietors, this is best practice for clean bookkeeping and accurate Schedule C reporting. For LLC owners, it’s legally critical — a practice called “piercing the corporate veil” can occur when business and personal funds are mixed, which courts have used to void the limited liability protection entirely. Your LLC becomes meaningless if your business expenses are coming out of your personal checking account.

The practical setup: one business checking account for all client payments, one business savings account holding your 30% tax buffer. Every invoice gets paid into checking. Every Friday, 30% transfers automatically to savings. You never touch the savings account until quarterly estimated taxes are due.

For a full breakdown of how to calculate your tax buffer, set your Minimum Viable Income, and build your quarterly tax payment schedule, the freelance financial projections guide covers the exact math — including how your legal structure affects the numbers once you pursue an S-Corp election.

Clean expense tracking becomes more valuable at tax time than most freelancers expect. Home office deductions, software subscriptions, professional development, equipment — these all reduce your Schedule C net profit and therefore your self-employment tax exposure. Tracking them manually in a spreadsheet works early on and breaks down fast as your client count grows.

The honest downside on accounting software: QuickBooks raises its subscription prices regularly, and for a straightforward Sole Proprietor with five expense categories and three clients, the full interface feels like overkill — you’ll spend more time learning the platform than it saves you. If you’re early-stage and under $30k/year, Wave’s free tier handles basic invoicing and expense tracking without the learning curve or the monthly fee. QuickBooks earns its cost once deduction complexity and quarterly tax estimates become genuinely time-consuming to manage manually.

QuickBooks

Best for: Freelancers who have crossed $30k/year in revenue and need automated expense categorization, quarterly tax estimates, and a real P&L without hiring a bookkeeper.

Documenting Your Structure in Your Business Plan

Your legal structure isn’t a background administrative detail — it’s a foundational business decision that affects your pricing, your tax buffer, your banking setup, and your liability exposure. It belongs in your business plan, documented and visible.

In the 1-page Notion framework, your structure choice sits in the “Operations” block alongside your tech stack and banking setup. It’s a single line: “Currently operating as: [Sole Proprietor / Single-Member LLC]. LLC formation target: [trigger condition or date].”

That target condition keeps the decision active rather than something you set and forget. When you hit your revenue trigger, the plan reminds you. The freelance business plan guide shows you exactly where this block fits within the full 1-page framework and how to connect it to your financial targets.

🎁 Free Digital Asset: 1-Page Business Plan

Download the 1-page Notion business plan template and document your legal structure and upgrade trigger today.

Frequently Asked Questions

Do I legally need an LLC to freelance?

No — and this misconception stops more people from starting than almost anything else. You can legally operate, send invoices, sign contracts, and receive payments under your own name as a Sole Proprietor from day one. An LLC is a tool for asset protection, not legal permission to work.

The only things an LLC changes are your liability exposure and, eventually, your tax optimization options. If you’re waiting to form an LLC before you start freelancing, stop waiting and start pitching.

Does an LLC save freelancers money on taxes?

A standard Single-Member LLC does not reduce your income tax or self-employment tax at all. The IRS treats it as a disregarded entity by default — your taxes work exactly the same as a Sole Proprietor. The tax advantage only arrives when you elect S-Corporation tax status, which requires running a formal payroll and paying yourself a “reasonable salary.”

That administrative overhead only makes financial sense once your net profit consistently exceeds $60,000–$80,000 annually. Below that threshold, the cost of S-Corp compliance typically exceeds the tax savings. Talk to a CPA before making that election — the break-even point varies significantly based on your state, your income, and your deduction profile.

Can I start as a Sole Proprietor and change to an LLC later?

Yes, and this is the path I recommend for the vast majority of new freelancers. Starting as a Sole Proprietor costs nothing, removes all formation friction, and lets you validate your offer and land paying clients before you spend a dollar on legal structure. You can convert to an LLC at any point — there’s no penalty, no complicated legal process, and no gap in your ability to operate.

When your revenue trigger hits or your risk profile increases, file the LLC paperwork in your state, open a dedicated business account, and update your contracts and invoices to reflect the new entity name. The transition takes a few days, not months.

The Verdict & Final Action Step

Start as a Sole Proprietor today. Remove all friction between you and your first paying client. Don’t let legal structure become another reason to delay launching.

Then set a clear upgrade trigger — a specific revenue milestone or contract type — and write it into your business plan so it’s a committed decision, not a vague intention. When you hit the trigger, file the LLC paperwork. It costs less than one hour of your billing rate in most states and protects everything you’ve built.

Action beats perfection at every stage of a freelance business. The best legal structure is the one that matches where you actually are right now, not where you hope to be in two years.

Verdict: Start as a Sole Proprietor, validate your offer, and land your first clients without spending a dollar on formation. Set a revenue trigger of $1,000–$2,000/month consistent income as your LLC upgrade signal. When you hit it, file the paperwork, open the business account, and protect what you’ve built. Download the 1-page Notion business plan template, document your structure choice, and set your upgrade trigger today.

Complete 2026 Methodology: Creating an Agile Freelance Business Plan

Your legal structure is one decision inside a larger operating system. It connects directly to your tax buffer calculations, your banking setup, your contract language, and your long-term wealth-building strategy.

Helping independent contractors navigate these high-stakes transitions safely is the core mission behind Smart Remote Gigs. Don’t let legal anxiety paralyze your progress. Get the structure right for where you are now. Build the plan that grows with you. That’s the whole methodology.