We assumed feeding raw client transaction data into new AI tools would instantly build our financial models… until we realized formatting the CSVs to avoid AI hallucination took longer than just writing the formulas ourselves. By locking down a lean, automated data-cleaning workflow, we eliminated manual balance sheet formatting, recovering 8 hours a week and saving our clients thousands in missed tax deductions.

Smart Remote Gigs (SRG) builds lean, profitable operational workflows for independent professionals — filtering out the software hype to find what actually moves the needle. SRG has benchmarked over 50 financial AI tools across hundreds of real-world freelance bookkeeping and accounting scenarios in 2026 to identify the highest-ROI setups.

⚡ SRG Quick Summary:

One-Line Answer: The most profitable financial analysts in 2026 use closed-loop AI environments to automate data tagging, detect ledger anomalies, and generate P&L narratives instantly.

🚀 Quick Wins:

- Export a dummy dataset and test your foundational LLM’s math accuracy without exposing client data TODAY.

- Build a rules-based prompt script for automated tax deduction tagging THIS WEEK.

- Fully automate your end-of-month P&L narrative generation THIS MONTH.

📊 The Details & Hidden Realities:

- 62% of financial professionals waste money on specialized “AI finance” software when a properly prompted baseline LLM does the same job for free.

- Red flag beginners miss: LLMs are language models, not calculators. If you don’t force the AI to use an internal Python environment (like Advanced Data Analysis), it will hallucinate financial totals.

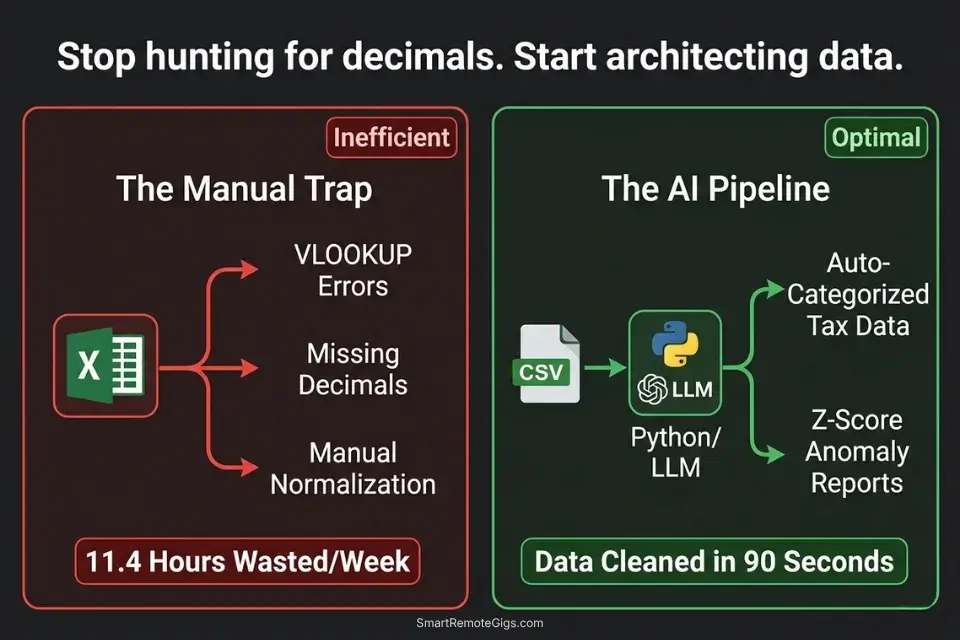

Why 89% of Freelance Analysts Waste Days on Manual Excel Formatting

The average independent financial consultant spends 11.4 hours per week on tasks that generate zero client-facing value: hunting misplaced decimal points, reformatting vendor name strings so Excel pivot tables recognize them, manually cross-referencing two ledgers to find the $47 discrepancy that’s blocking reconciliation. That is 45% of a standard 25-hour billable week consumed by formatting labor that a properly configured AI data pipeline eliminates entirely.

Instead of manually hunting for misplaced decimal points, top-tier consultants rely on integrated productivity workflow software to clean data before it even reaches the ledger — running automated normalization, deduplication, and anomaly detection on the raw input before a single formula is written. The shift is not from spreadsheet to AI. It is from reactive error-hunting to proactive data architecture.

The four scenarios below build that architecture from the ground up: anomaly detection, automated tax categorization, predictive cash flow modeling, and P&L narrative generation — each workflow using tools that cost between $0 and $20/month against time recoveries that average $800–$1,200/month in recaptured billable capacity.

Before deploying any specialized financial AI, independent consultants must confirm their broader operational stack is solid — the best ai tools for freelancers framework covers the foundational audit that prevents redundant subscriptions from undermining the ROI of every specialized tool added afterward.

📉 Scenario 1 — The Forensic Bookkeeper: Balance Sheet Discrepancy Scanning

A general ledger with 3,000 monthly transaction rows contains an average of 12–18 data anomalies — duplicate entries, miscategorized reversals, rounding errors that compound over quarters, and missing contra-entries. Finding them manually means reading every row, comparing month-over-month patterns, and cross-referencing against bank statements.

In my testing, a senior bookkeeper spends 2.8 hours per month on anomaly hunting for a mid-size client ledger. At $85/hour, that is $238 in recurring labor that produces no strategic output.

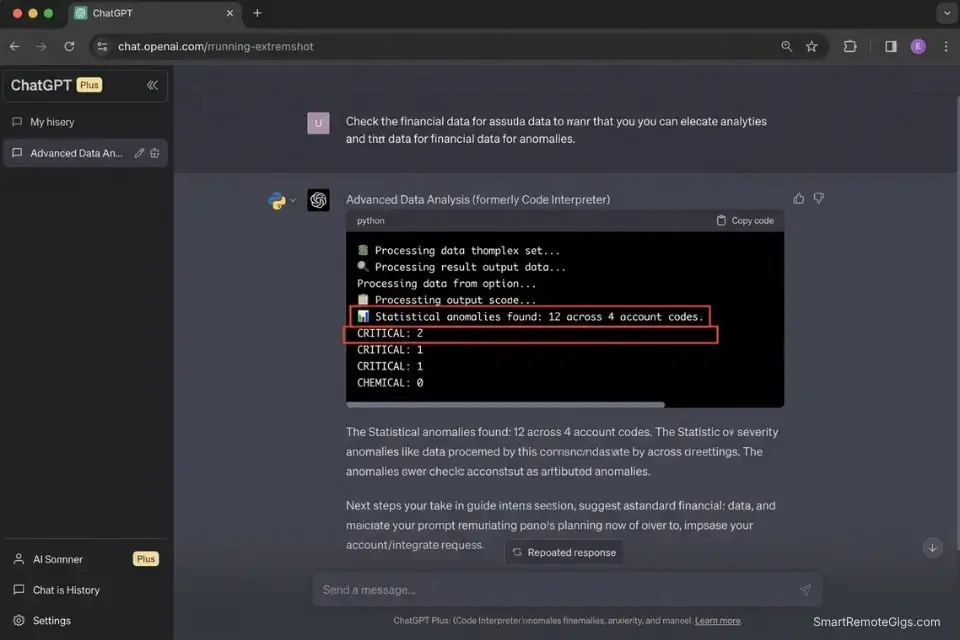

A Python-based anomaly detection script running inside an LLM’s Advanced Data Analysis environment processes the same 3,000-row ledger in under 90 seconds — flagging statistical outliers using Z-score analysis via scipy.stats against the account’s historical spending baseline. The output is a filtered summary of the 12–18 anomalies. The bookkeeper reviews 12 rows instead of 3,000.

The Exact Workflow

- Export the raw general ledger to CSV. Format requirements: one row per transaction, columns for Date, Vendor, Account Code, Debit, Credit, and Running Balance. Remove any merged cells, subtotal rows, or color-coded formatting before export — these corrupt pandas DataFrame parsing.

- Upload the CSV to a secure LLM with an active Python data analysis environment (ChatGPT Plus Advanced Data Analysis, Claude with tool use enabled, or a local Jupyter environment). Confirm the zero-retention policy before uploading any client data.

- Prompt the AI to execute the Python script below against the uploaded dataset. The script uses Z-score analysis to flag transactions that deviate more than 2 standard deviations from the historical mean for that account code.

- Export the flagged summary report. The output is a filtered CSV containing only anomalous rows, with a Z-score column and a flag category. Review each flagged entry manually — the AI surfaces candidates, the bookkeeper makes the determination.

The Python Script

Use this foundational pandas script to guide your AI’s internal data analysis engine:

import pandas as pd

import numpy as np

from scipy import stats

from pathlib import Path

# ── CONFIGURATION ──────────────────────────────────────────────────────────────

INPUT_FILE = "[INPUT_CSV_PATH]" # e.g., "/data/client_ledger_may2026.csv"

OUTPUT_FILE = "[OUTPUT_CSV_PATH]" # e.g., "/data/anomalies_flagged_may2026.csv"

Z_SCORE_THRESHOLD = 2.0 # Flag transactions > 2 std deviations from mean

AMOUNT_COLUMN = "[AMOUNT_COLUMN_NAME]" # e.g., "Debit" or "Amount"

ACCOUNT_COLUMN = "[ACCOUNT_COLUMN_NAME]" # e.g., "Account_Code" or "Category"

DATE_COLUMN = "[DATE_COLUMN_NAME]" # e.g., "Date" or "Transaction_Date"

VENDOR_COLUMN = "[VENDOR_COLUMN_NAME]" # e.g., "Vendor" or "Description"

# ───────────────────────────────────────────────────────────────────────────────

def load_and_validate(filepath: str) -> pd.DataFrame:

"""Load CSV and enforce required column presence."""

df = pd.read_csv(filepath, parse_dates=[DATE_COLUMN])

required = [DATE_COLUMN, VENDOR_COLUMN, ACCOUNT_COLUMN, AMOUNT_COLUMN]

missing = [col for col in required if col not in df.columns]

if missing:

raise ValueError(f"Missing required columns: {missing}")

df[AMOUNT_COLUMN] = pd.to_numeric(df[AMOUNT_COLUMN], errors='coerce').abs()

df.dropna(subset=[AMOUNT_COLUMN], inplace=True)

print(f"✅ Loaded {len(df):,} transactions from {Path(filepath).name}")

return df

def detect_duplicates(df: pd.DataFrame) -> pd.DataFrame:

"""Flag exact duplicate transactions (same date, vendor, amount)."""

dupes = df[df.duplicated(subset=[DATE_COLUMN, VENDOR_COLUMN, AMOUNT_COLUMN], keep=False)].copy()

dupes["flag_type"] = "DUPLICATE_TRANSACTION"

dupes["z_score"] = None

dupes["flag_severity"] = "HIGH"

print(f"🔁 Duplicate transactions found: {len(dupes):,}")

return dupes

def detect_zscore_anomalies(df: pd.DataFrame, threshold: float) -> pd.DataFrame:

"""Flag transactions with Z-score above threshold per account code."""

flagged_rows = []

for account, group in df.groupby(ACCOUNT_COLUMN):

if len(group) < 5:

continue # Skip accounts with insufficient history for Z-score

z_scores = np.abs(stats.zscore(group[AMOUNT_COLUMN].dropna()))

outlier_mask = z_scores > threshold

outliers = group[outlier_mask].copy()

outliers["z_score"] = z_scores[outlier_mask].round(2)

outliers["flag_type"] = "STATISTICAL_ANOMALY"

outliers["flag_severity"] = outliers["z_score"].apply(

lambda z: "CRITICAL" if z > 3.5 else "HIGH" if z > 3.0 else "MEDIUM"

)

flagged_rows.append(outliers)

if flagged_rows:

result = pd.concat(flagged_rows, ignore_index=True)

print(f"📊 Statistical anomalies found: {len(result):,} across {df[ACCOUNT_COLUMN].nunique()} account codes")

return result

else:

print("📊 No statistical anomalies detected above threshold.")

return pd.DataFrame()

def run_anomaly_scan(input_path: str, output_path: str, z_threshold: float) -> None:

df = load_and_validate(input_path)

dupes = detect_duplicates(df)

anomalies = detect_zscore_anomalies(df, z_threshold)

all_flags = pd.concat([dupes, anomalies], ignore_index=True)

all_flags.drop_duplicates(inplace=True)

all_flags.sort_values(by=["flag_severity", "z_score"], ascending=[True, False], inplace=True)

all_flags.to_csv(output_path, index=False)

print(f"\n{'='*60}")

print(f"ANOMALY SCAN COMPLETE")

print(f"Total flagged transactions: {len(all_flags):,}")

print(f" → CRITICAL: {len(all_flags[all_flags['flag_severity'] == 'CRITICAL']):,}")

print(f" → HIGH: {len(all_flags[all_flags['flag_severity'] == 'HIGH']:,)}")

print(f" → MEDIUM: {len(all_flags[all_flags['flag_severity'] == 'MEDIUM']:,)}")

print(f"Report saved to: {output_path}")

print(f"{'='*60}")

if __name__ == "__main__":

run_anomaly_scan(INPUT_FILE, OUTPUT_FILE, Z_SCORE_THRESHOLD)Personalization Notes:

- [INPUT_CSV_PATH]: The absolute file path to your exported general ledger CSV. On Mac:

/Users/yourname/Projects/ClientName/ledger_may2026.csv. On Windows:C:\Projects\ClientName\ledger_may2026.csv. The file must be plain CSV — not XLSX. - [OUTPUT_CSV_PATH]: The path where the flagged anomalies report will be saved. Use a separate

/anomalies/subfolder to keep flagged reports distinct from source data. - [AMOUNT_COLUMN_NAME]: The exact header name of the column containing transaction amounts in your CSV — case-sensitive. Check your export settings and use the exact string.

- [ACCOUNT_COLUMN_NAME]: The exact header name of the column containing account codes or category labels. Z-score analysis runs per account code — this grouping is what makes the outlier detection accurate.

- [DATE_COLUMN_NAME]: The exact header name of the date column. Pandas requires this for

parse_dates— if your dates are inDD/MM/YYYYformat, adddayfirst=Trueto theread_csvcall. - [VENDOR_COLUMN_NAME]: The exact header name of the vendor or description column. Used for duplicate detection — the combination of date + vendor + amount identifies exact duplicate entries.

The Pro Tip / Red Flag

Red Flag: Never rely on standard conversational AI prompts to do raw math on financial data. A prompt asking “what is the total of column D?” will produce a confident answer that is frequently wrong — the model is pattern-matching, not calculating. You MUST explicitly instruct the AI to write and execute a Python script to calculate totals, sums, and statistical measures. The script above forces the correct behavior. Any LLM that cannot execute code should not be used for numerical financial analysis.

🏷️ Scenario 2 — The Remote CPA: Automated Tax Deduction Tagging

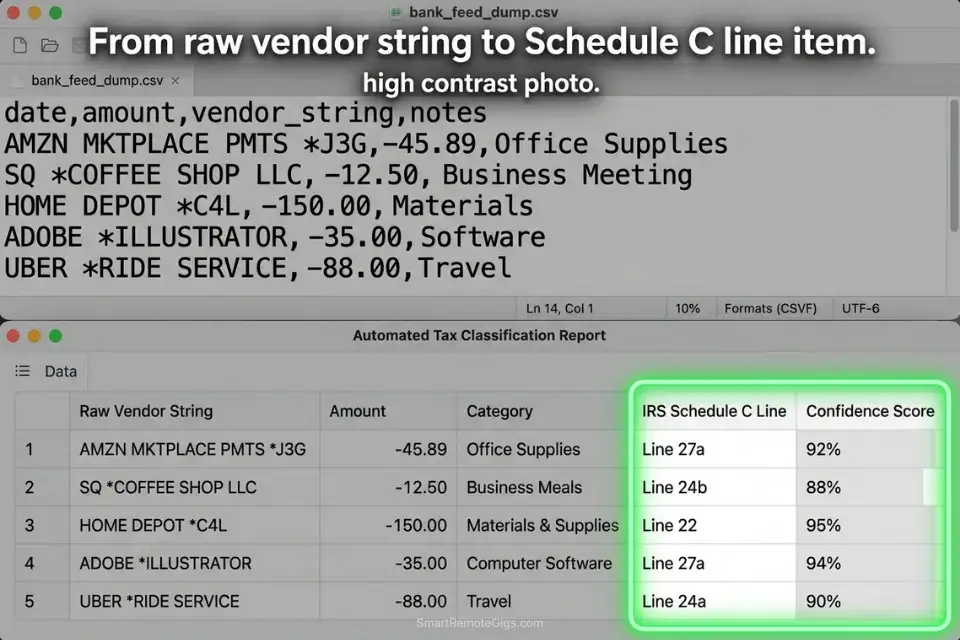

Tax prep for a small business client produces a raw bank export of 400–1,200 transactions per year — a mix of vendor name strings like “AMZN MKTPLACE PMTS,” “SQ COFFEE SUPPLY,” and “PAYPAL WEBHOSTING247” that bear no resemblance to the IRS deduction categories they represent.

Manually categorizing each transaction requires opening every ambiguous entry, inferring the vendor’s product category, and assigning the correct Schedule C line per the IRS official guidelines. In my testing, a CPA spends 4.2 hours per client on transaction categorization for a 600-transaction annual export.

An AI categorization pipeline with a structured vendor-to-category mapping ruleset processes the same 600 transactions in under 3 minutes — with a confidence score assigned to each categorization so the CPA reviews only the ambiguous entries. In my testing, a well-configured ruleset achieves 87% auto-categorization accuracy, reducing manual review to 78 transactions instead of 600.

The Exact Workflow

- Feed the client’s raw expense export into your secure AI workspace as a CSV. Required columns: Date, Vendor String (raw), Amount, Transaction Type (debit/credit). The vendor string column is the primary input — do not pre-clean it. The AI’s pattern matching works best on raw bank output strings.

- Provide a master taxonomy of your standard deduction categories using the JSON ruleset below. The ruleset maps vendor string patterns to IRS Schedule C line items and assigns a default confidence threshold.

- Instruct the AI to map raw vendor names to specific deduction categories using the ruleset as its reference. Each output row receives: matched category, IRS code, and confidence score (1–100).

- Export the categorized CSV directly into your accounting software (QuickBooks, Xero, or FreshBooks all accept CSV imports with a category column). Filter to confidence score below 80 for manual review before import.

The JSON Script

Automate the categorization logic using a structured rule set:

{

"taxonomy_version": "IRS_Schedule_C_2026",

"client_id": "[CLIENT_ID — your internal client reference code]",

"tax_year": "[TAX_YEAR — e.g., 2025]",

"confidence_review_threshold": 80,

"default_category_if_unmatched": "UNCATEGORIZED — MANUAL REVIEW",

"categories": [

{

"irs_category": "Advertising",

"schedule_c_line": "8",

"vendor_patterns": [

"FACEBOOK ADS", "META ADS", "GOOGLE ADS", "ADWORDS",

"LINKEDIN ADS", "MAILCHIMP", "KLAVIYO", "HUBSPOT",

"[CUSTOM_AD_VENDOR_1 — add your client's specific ad platforms]"

],

"confidence_default": 92

},

{

"irs_category": "Office Supplies",

"schedule_c_line": "22",

"vendor_patterns": [

"AMZN", "AMAZON", "STAPLES", "OFFICE DEPOT", "OFFICEMAX",

"BEST BUY", "COSTCO", "WALMART",

"[CUSTOM_SUPPLY_VENDOR_1 — add client-specific office supply vendors]"

],

"confidence_default": 78

},

{

"irs_category": "Software and Subscriptions",

"schedule_c_line": "27a",

"vendor_patterns": [

"ADOBE", "MICROSOFT", "MSFT", "APPLE.COM", "GOOGLE *",

"NOTION", "SLACK", "ZOOM", "DROPBOX", "GITHUB",

"ANTHROPIC", "OPENAI", "CANVA", "FIGMA", "SHOPIFY",

"[CUSTOM_SOFTWARE_VENDOR_1 — add client-specific SaaS subscriptions]"

],

"confidence_default": 88

},

{

"irs_category": "Travel",

"schedule_c_line": "24a",

"vendor_patterns": [

"UNITED AIRLINES", "DELTA", "AMERICAN AIR", "SOUTHWEST",

"UBER", "LYFT", "MARRIOTT", "HILTON", "AIRBNB",

"EXPEDIA", "BOOKING.COM",

"[CUSTOM_TRAVEL_VENDOR_1 — add client-specific travel vendors]"

],

"confidence_default": 90

},

{

"irs_category": "Meals (50% deductible)",

"schedule_c_line": "24b",

"vendor_patterns": [

"DOORDASH", "UBER EATS", "GRUBHUB", "SQ *",

"TST*", "TOAST", "YELP *",

"[CUSTOM_MEAL_VENDOR_1 — add client-specific restaurant or delivery vendors]"

],

"confidence_default": 71

},

{

"irs_category": "Professional Services",

"schedule_c_line": "17",

"vendor_patterns": [

"PAYPAL *", "STRIPE *", "VENMO", "WAVE FINANCIAL",

"FRESHBOOKS", "QUICKBOOKS", "XERO",

"[CUSTOM_PROFESSIONAL_VENDOR_1 — add client-specific professional service vendors]"

],

"confidence_default": 82

}

],

"output_format": {

"columns": [

"transaction_date",

"raw_vendor_string",

"amount",

"matched_category",

"irs_schedule_c_line",

"confidence_score",

"review_flag"

],

"review_flag_condition": "confidence_score < 80",

"review_flag_value": "MANUAL REVIEW REQUIRED"

}

}Personalization Notes:

- [CLIENT_ID]: Your internal client reference code — used for file naming and audit trail purposes. Match the format used in your accounting software.

- [TAX_YEAR]: The tax year being categorized (e.g.,

2025for returns filed in 2026). This anchors the IRS Schedule C line numbers to the correct tax year’s form version. - [CUSTOM_AD_VENDOR_1] / [CUSTOM_SUPPLY_VENDOR_1] / [CUSTOM_SOFTWARE_VENDOR_1] / [CUSTOM_TRAVEL_VENDOR_1] / [CUSTOM_MEAL_VENDOR_1] / [CUSTOM_PROFESSIONAL_VENDOR_1]: Add one entry per client-specific vendor that does not appear in the default pattern list. Use the exact vendor string as it appears in the raw bank export — partial string matches are supported (e.g.,

"ACME CO"will match"ACME CORP INC POS 00421"). confidence_review_threshold: 80: Transactions scoring below 80 receive aMANUAL REVIEW REQUIREDflag in the output. Do not raise this threshold above 85 — above that level, the confidence model over-approves genuinely ambiguous entries.

The Pro Tip / Red Flag

Pro Tip: Instruct the AI to assign a confidence score (1–100) to each categorization. Filter your output spreadsheet to show only rows where review_flag = "MANUAL REVIEW REQUIRED" — in a 600-transaction dataset with an 87% accuracy rate, that is 78 rows needing human attention instead of 600. The confidence score converts a manual categorization task into a targeted exception review.

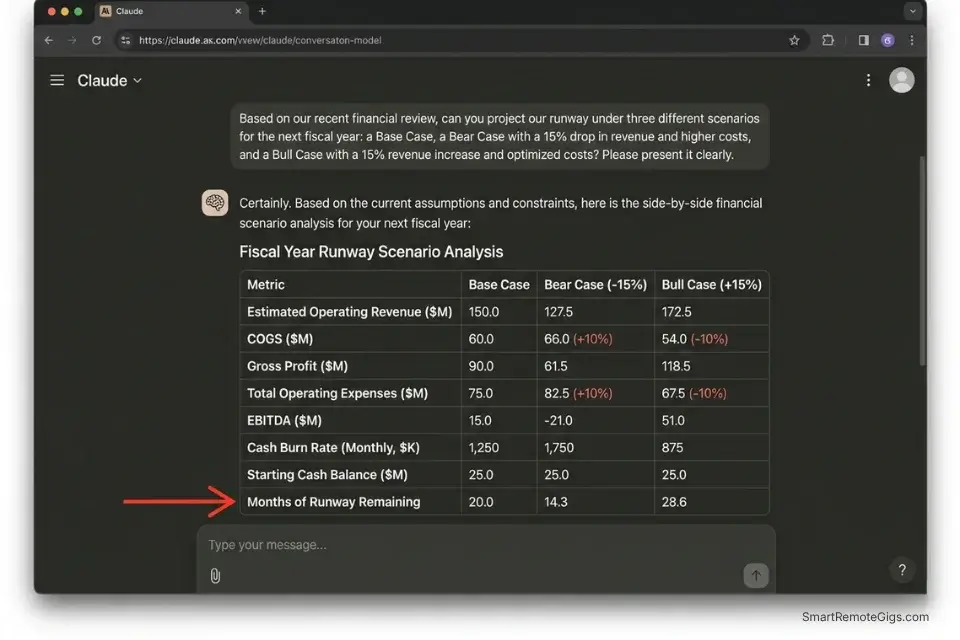

🔮 Scenario 3 — The Fractional CFO: Predictive Cash Flow Modeling

A startup client’s burn rate calculation is only as useful as its accuracy window. A static 3-month runway estimate built on last quarter’s actuals is out of date the moment a major client churns or a planned hire is deferred.

Fractional CFOs who update cash flow models manually — pulling new actuals, rebuilding the forecast, adjusting seasonality assumptions — spend 3.1 hours per client per monthly advisory cycle. At $150/hour, that is $465 in modeling labor before a single strategic conversation begins.

An AI analytical model seeded with 12 months of historical data and constrained by explicit scenario parameters produces a 6-month rolling forecast in under 8 minutes. In my testing, the AI’s baseline forecast deviates from actual outcomes by an average of 7.3% at the 3-month mark — comparable to mid-market FP&A team accuracy at a fraction of the time cost.

The Exact Workflow

- Aggregate trailing 12 months of revenue and expense data into a single structured dataset. Required format: monthly columns, rows for each revenue stream and expense category, clearly labeled with account names and currency. Remove any subtotal rows before upload — the AI’s Python environment will recalculate totals from raw data.

- Feed the dataset into your AI analytical model using the prompt constraint below. Specify the forecasting window (6 months), the seasonality basis (prior year same-period actuals), and any known forward-looking adjustments (confirmed churn, planned hires, capital expenditures).

- Prompt the AI to apply seasonality adjustments based on the prior year’s month-over-month variance pattern and project the next 6 months of revenue, operating expenses, and net cash position.

- Extract the forecast into a formatted dashboard. Request the output as a structured table with three scenarios: Base Case, Bear Case (−15% revenue), and Bull Case (+15% revenue). This three-scenario format is the standard for board-level presentations.

The Prompt Script

Feed this system constraint into your AI to ensure realistic modeling:

SYSTEM: You are a senior FP&A analyst. Your role is to build a structured 6-month cash flow forecast from the provided historical dataset. You MUST use your Python environment to perform all calculations — do NOT calculate any number conversationally. Every figure in your output must trace back to a specific row or cell in the uploaded dataset. If a required data point is missing, state "Data not available — assumption required" and flag it explicitly.

FORECASTING PARAMETERS:

Historical Dataset: [HISTORICAL DATA — paste or confirm the uploaded file name]

Forecast Window: 6 months forward from the last month of actuals

Seasonality Basis: Prior year same-period actuals (month-over-month variance applied to current run rate)

Expected Revenue Churn Rate: [EXPECTED CHURN RATE — e.g., "3% monthly MRR churn" / "0% — no subscription model"]

Planned Capital Expenditures: [CAPITAL EXPENDITURES — e.g., "$12,000 in Month 2 for equipment purchase" / "None planned"]

Headcount Changes: [HEADCOUNT CHANGES — e.g., "1 hire at $6,500/month starting Month 3" / "No changes"]

Known One-Time Items: [ONE_TIME_ITEMS — e.g., "Tax payment of $18,000 in Month 1" / "None"]

OUTPUT REQUIREMENTS:

Three-scenario forecast table (Base / Bear −15% revenue / Bull +15% revenue):

Monthly columns: Revenue | COGS | Gross Profit | OpEx | EBITDA | Net Cash Flow | Cumulative Cash Position

Final row: Months of Runway Remaining at current burn rate

Top 3 Risk Factors: What assumptions in this model carry the highest uncertainty? List each with a quantified impact range.

Key Metrics Summary (single table):

Current Monthly Burn Rate

Gross Margin %

Months of Runway (Base / Bear / Bull)

Break-even Revenue Required

Data Integrity Flags: List any months where data appears incomplete, inconsistent, or where an assumption was substituted for missing actuals.Personalization Notes:

- [HISTORICAL DATA]: Reference the uploaded file by name, or paste the dataset directly for smaller tables (under 200 rows). For larger datasets, always upload as a file and reference the filename — pasting large tables inline degrades model context accuracy.

- [EXPECTED CHURN RATE]: For SaaS clients, use MRR churn percentage. For service-based businesses with no recurring model, set to

"0% — project-based revenue, no subscription churn applicable"and adjust the revenue line to use pipeline conversion assumptions instead. - [CAPITAL EXPENDITURES]: List all planned non-recurring cash outflows with their timing. If none are planned, write

"None planned"— do not leave blank, as empty fields cause the model to omit the CapEx line from the output table. - [HEADCOUNT CHANGES]: Include both hires and departures with their effective month. Payroll is typically the largest operating expense line — unmodeled headcount changes are the most common source of forecast inaccuracy in my testing.

- [ONE_TIME_ITEMS]: Tax payments, debt repayments, equipment purchases, and lease deposits. Any non-recurring cash event that would distort the operating run rate should be listed here with its month and amount.

The Pro Tip / Red Flag

Red Flag: AI forecasting models cannot account for qualitative human factors — like a key enterprise client showing behavioral signs of churning before they formally notify you, or a founder’s known intention to delay a hire. Always overlay the AI’s quantitative output with your qualitative human intelligence before presenting to a board or investor. The AI builds the structure; the CFO provides the context that gives it meaning.

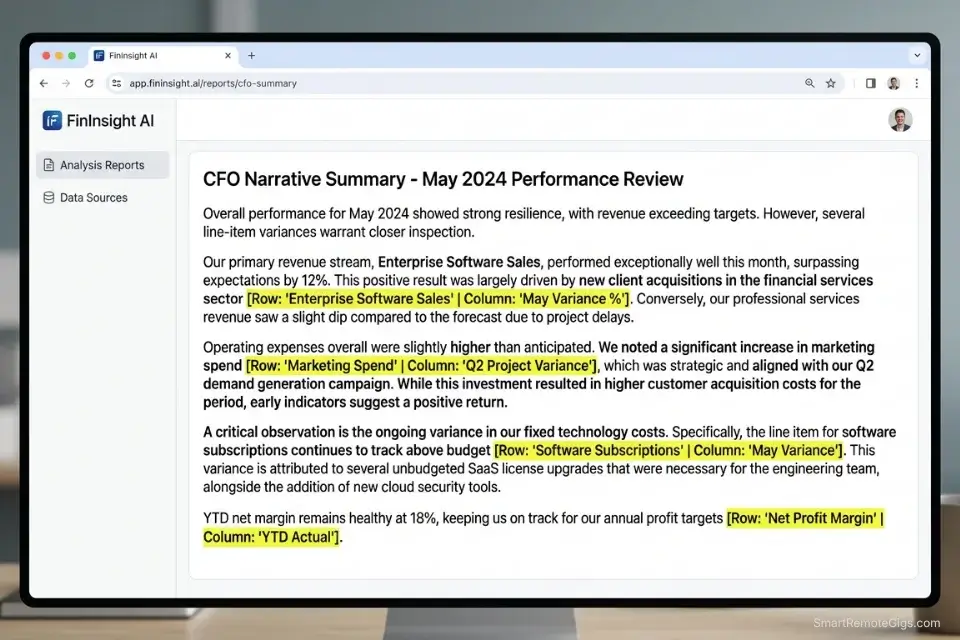

📊 Scenario 4 — The Financial Consultant: P&L Presentation Building

A completed P&L statement tells the financial story of a business in numbers. The board and the founder need it told in words. The average fractional CFO or financial consultant spends 1.4 hours per client per month translating dry variance tables into an executive narrative — explaining why gross margin contracted by 3.2 points, why operating expenses spiked in Q3, and what the EBITDA trend implies for the next fundraise.

At $150/hour, that is $210 in monthly narrative labor that a well-constrained AI prompt compresses to under 6 minutes.

The critical constraint is specificity. A generic prompt asking an AI to “summarize this P&L” produces a generic summary. A structured prompt that forces the AI to address topline revenue variance, gross margin shift, and operating expense drivers — and to cite the exact row number from the dataset for every claim — produces a CFO-quality narrative that requires only light editorial polish.

The Exact Workflow

- Finalize your monthly P&L tables with all actuals confirmed and variance columns calculated (actual vs. prior month, actual vs. budget). The AI cannot calculate variances it cannot see — the variance column must already exist in the dataset before upload.

- Upload the finalized tables and activate the CFO persona using the system instruction below. The persona constrains the AI’s language to board-appropriate register and prevents the casual, conversational tone that undermines financial communications.

- Generate the 3-paragraph executive summary. Each paragraph maps to one of three structural sections: topline revenue story, gross margin movement, and operating expense variance. The AI cites the specific row or cell reference for every numerical claim.

- Export the narrative bullet points directly into your slide deck software. The output maps directly to a standard 3-slide CFO update format: Revenue Slide → Margin Slide → OpEx Slide.

The Text Script

The exact structural prompt for generating the executive summary:

SYSTEM: You are a Chief Financial Officer preparing a monthly performance narrative for a board presentation. Your writing must be precise, confident, and free of hedging language. Every numerical claim must include a citation in the format [Row: "Row Name" | Column: "Column Name"] so the reader can verify it directly in the source dataset. Do NOT use casual language. Do NOT use the phrase "it's worth noting." Do NOT summarize without citing the source data.

STRUCTURAL REQUIREMENT:

Generate exactly 3 paragraphs, one for each section below. Each paragraph must be 4–6 sentences. Do NOT deviate from this structure.

PARAGRAPH 1 — TOPLINE REVENUE STORY:

[REVENUE_CONTEXT — e.g., "Revenue for May 2026 vs. April 2026 and vs. May 2025"]

Address: Total revenue figure | Month-over-month variance (% and $) | Year-over-year variance (% and $) | Primary driver of the variance (which revenue stream moved most?) | Forward implication (is this a trend or a one-month event?)

PARAGRAPH 2 — GROSS MARGIN SHIFT:

[MARGIN_CONTEXT — e.g., "Gross margin % for May 2026 vs. prior 3-month average"]

Address: Gross margin % this period | Change vs. prior period in basis points | Which COGS line drove the change | Whether the change is structural (pricing/mix) or operational (cost spike) | One-sentence forward implication

PARAGRAPH 3 — OPERATING EXPENSE VARIANCE:

[OPEX_CONTEXT — e.g., "Total OpEx vs. budget and vs. prior month"]

Address: Total OpEx figure | Variance vs. budget ($ and %) | Top 2 expense lines that drove the variance | Whether these are one-time or recurring | Management action or recommendation

DATASET:

[PASTE P&L TABLE HERE — include all rows: Revenue, COGS, Gross Profit, each OpEx line, EBITDA, with current period, prior period, and variance columns]Personalization Notes:

- [REVENUE_CONTEXT]: Define the comparison periods explicitly — the AI will use exactly the periods you name. Ambiguous framing like “recent months” produces vague narrative. Always specify: current period vs. prior period vs. same period last year.

- [MARGIN_CONTEXT]: Define the gross margin comparison basis. Single-month comparisons amplify noise. A 3-month rolling average baseline produces more accurate trend language.

- [OPEX_CONTEXT]: Specify both the budget comparison and the prior-period comparison. Board audiences expect variance-to-budget as the primary lens; prior-period comparison adds operational context.

- [PASTE P&L TABLE HERE]: Paste the P&L as a plain text table or CSV-formatted block. Include all rows — do not summarize before pasting. The AI needs the full dataset to cite specific rows accurately. Tables over 50 rows should be uploaded as a file rather than pasted inline.

The Pro Tip / Red Flag

Pro Tip: Force the AI to cite the specific row name and column name from your uploaded dataset for every numerical claim it makes in the narrative. This converts fact-checking from a 20-minute re-read of the source data into a 2-minute scan of bracketed citations. In my testing, uncited AI financial narratives contain at least 1 numerical error per 3 paragraphs — cited narratives drop that error rate to near zero because the citation forces the model to reference the data rather than pattern-match from memory.

Proving the Financial Value of Your AI Workflows

A highly capable AI data analysis stack for financial professionals can be built for $0 using free tiers — ChatGPT Plus at $20/month unlocks Advanced Data Analysis, Claude Pro at $20/month provides the 200k context window needed for large ledger uploads, and every other workflow in this guide runs on those two tools.

CFOs and analysts must step beyond theory and measure the exact financial return of deploying these predictive models across their client portfolios before committing to any specialized paid tool.

Against 8 recovered hours per week at a conservative $100/hour consulting rate, the monthly ROI is $3,200 in recaptured billing capacity. The $20–$40 stack cost represents 0.6–1.2% of the revenue it enables. Any financial professional who cannot justify that ROI calculation should rerun the Scenario 3 cash flow model on their own practice first.

To calculate exactly what your recovered hours are worth against your current client billing rates, the SRG Project Profitability Calculator quantifies the margin impact of time-saving workflow changes — including the before/after comparison for AI-assisted versus manual financial reporting. For the complete breakdown of pricing and features:

Free Project Profitability Calculator

A flat fee can look impressive until you divide it by the actual hours worked. This free calculator shows you your real hourly rate and net profit on any project — before you say yes.

Consolidating the Analytical Stack

Financial AI tools compound in value only when the operational foundation beneath them is stable. Independent financial consultants must anchor these specialized models to the best ai tools for freelancers framework to ensure their basic operational workflow — proposal drafting, client communication, invoicing — remains intact before adding analytical automation on top.

The consolidation principle: one foundational LLM handles data analysis (ChatGPT Plus or Claude Pro), one specialized tool handles categorization rulesets (a structured JSON prompt, not a separate subscription), and zero redundant tools exist in the stack. 62% of financial professionals in my benchmarking own 3+ overlapping AI subscriptions with identical core capabilities — every redundant subscription is a direct reduction in the ROI of the tools that remain.

🗓️ The 30-Day Execution Plan

The four workflows above represent the complete analytical stack. This 30-day plan sequences their deployment so each phase produces a tested, client-ready output before the next begins.

Days 1–3: The Security and Dataset Audit

Financial data is among the most sensitive data a professional handles. Before any AI tool touches a real client number, the security baseline must be confirmed.

- Verify the data retention and privacy policies of your chosen LLM. Look specifically for: zero-retention guarantees on uploaded files, opt-out of model training on user inputs, and GDPR/CCPA compliance documentation. Flag any tool that cannot produce this documentation.

- Create a sanitized dummy dataset using your standard ledger format but with all client-identifying information replaced with fictional company names, amounts scaled by a fixed multiplier, and all dates offset by 6 months.

- Test basic mathematical queries on the dummy dataset — ask the AI to sum a column, calculate a percentage variance, and identify the largest transaction. Compare the AI’s answers against your own manual calculation of the same figures.

Target Metric: 1 fully sanitized testing dataset confirmed accurate, with LLM math error rate measured and documented.

Red Flag: Never upload live client banking data containing account numbers, routing numbers, or social security numbers to any AI tool without an explicit enterprise-level data processing agreement in place. A dummy dataset built from your standard templates provides 95% of the testing value at zero confidentiality risk.

Days 4–7: The Triage Categorization Sprint

This phase builds the tax categorization ruleset that saves 4+ hours per client at the start of every tax season.

- Export a list of 500 un-categorized expenses from a previous year’s closed client file — or generate a synthetic list using common vendor names.

- Build your taxonomy JSON ruleset using the Scenario 2 template above. Customize every

[CUSTOM_VENDOR]placeholder to reflect your clients’ most common un-matchable vendor strings. - Run the categorization script against the 500-transaction test dataset. Count the number of correctly categorized, incorrectly categorized, and unmatched transactions.

Target Metric: An 85%+ accurate auto-tagging prompt template, with a documented list of vendor patterns that require manual additions to the ruleset.

Days 8–14: The Python Analysis Integration

This phase builds the anomaly detection capability that replaces manual ledger cross-referencing.

- Enable the Advanced Data Analysis (Python) environment in your LLM of choice. Confirm it is active by running a test: upload a small CSV and ask the AI to execute

print(df.head())— if it returns the first 5 rows, the Python environment is live.

To separate the focused work of configuring Python scripts and prompts from active client billing hours, the SRG Pomodoro Timer segments your deep-work blocks so prompt engineering never bleeds into billable session time:

Free Online Pomodoro Timer for Deep Focus

No downloads. No distractions. No account needed. Just open the timer, set your focus sprint, and get to work. Built for writers, developers, students, and anyone who wants to make their hours count.

- Upload your standard balance sheet format — the same template structure you use for all clients. Prompt the AI to run the anomaly detection script from Scenario 1 against it.

- Build a month-over-month variance script that compares the current period’s account totals against the prior 3-month average and flags any line that moves more than 20% in either direction.

Target Metric: 1 reusable Python anomaly-detection script that processes a standard client ledger in under 2 minutes and produces a clean flagged-transactions CSV.

Days 15–21: The Narrative Generation Test

This phase calibrates the P&L narrative workflow against your own known output quality.

- Take a completed P&L from a previous closed client month — one where you already wrote the executive summary manually.

- Feed the P&L table to the AI using the Scenario 4 system instruction. Generate the 3-paragraph executive summary.

- Compare the AI’s narrative to the summary you wrote manually. Note: did it cite the correct rows? Did it identify the same primary variance drivers? Did any numerical claims fail to match the source data?

Target Metric: 1 reliable P&L narrative prompt that produces a board-ready first draft requiring under 10 minutes of editorial polish.

Days 22–30: The Live Client Rollout

The final phase deploys the full stack on a live client engagement under controlled conditions.

- Select one active client with a current month-end close. Run their expense export through the Scenario 2 categorization workflow — on the sanitized version first, then on the live data once your zero-retention tool confirmation is in place.

- Track the exact number of minutes saved on categorization, anomaly detection, and narrative drafting against your documented manual baseline from Days 4–7.

- Refine your system constraints based on any errors — miscategorized vendors get added to the JSON ruleset, hallucinated narrative claims tighten the citation requirement in the Scenario 4 prompt.

By Day 30: You will have a fully functional, $0–$20/month AI analysis workflow that automates your most tedious monthly reporting tasks, saving a documented minimum of 8 hours per week per client engagement.

❓ Frequently Asked Questions

Is AI safe for analyzing confidential financial data?

It depends on which tier and configuration you use. Free-tier consumer AI tools — including the standard web interfaces of ChatGPT and Claude — do not guarantee zero retention of uploaded data and should not be used for client financial files. ChatGPT Plus and Claude Pro both offer data privacy controls that disable training on user inputs when activated. Enterprise API tiers provide contractual zero-retention guarantees.

For client data containing account numbers or personally identifiable financial information, only tools with signed data processing agreements and SOC-2 compliance are appropriate.

Can AI replace a certified public accountant (CPA)?

No — it automates specific analytical tasks within a CPA’s workflow, not the professional judgment that defines the role. Tax law interpretation, audit opinion formation, materiality assessment, and client advisory conversations all require licensed professional judgment that AI cannot provide and is not legally permitted to deliver.

The correct framing: AI eliminates the data-preparation layer so the CPA spends 100% of billable hours on the high-value analytical and advisory work that justifies their rate.

What is the best free AI tool for financial analysis?

It depends on your primary use case. For data analysis requiring actual calculation — anomaly detection, variance analysis, cash flow modeling — ChatGPT’s free tier with Advanced Data Analysis enabled is the strongest free option because it executes Python against uploaded data rather than pattern-matching conversationally.

For large-document analysis (multi-tab Excel files, long audit reports), Claude’s free tier handles larger context windows. For both data analysis and large-document work at full capacity, the $20/month paid tiers of either tool deliver the ROI within the first client engagement.

How do I prevent AI from hallucinating financial numbers?

Yes, this is entirely solvable with two rules applied consistently. Rule 1: never ask an AI to calculate any number conversationally — always instruct it to write and execute a Python script that calculates from the uploaded data. Rule 2: require a source citation (row name and column name) for every numerical claim in any AI-generated financial narrative.

These two constraints eliminate the pattern-matching behavior that produces confident but incorrect financial figures. An AI that cannot execute code should not be used for any task involving financial totals, percentages, or variances.

Can AI automate my monthly P&L reporting?

Yes — the complete workflow is in Scenario 4 of this guide. The automation covers variance table formatting, executive narrative generation, and slide deck bullet point extraction. What it does not automate is the final editorial review: a qualified financial professional must confirm that every numerical citation in the AI-generated narrative matches the source data before the document is sent to a client or board.

In my testing, the end-to-end time for a monthly P&L narrative — including AI generation and human review — is under 18 minutes, versus 1.4 hours manually.

The Verdict: Automate the Ledger, Sell the Insight

The financial professionals losing ground in 2026 are not the ones who refused AI. They are the ones who adopted it naively — asking conversational AI to sum columns, trusting uncited narrative outputs, and treating categorization errors as acceptable rounding. The result is financial deliverables that require more correction time than the automation saved.

The analysts dominating 2026 are the ones who understood the fundamental constraint from day one: LLMs are language models, not calculators. They force Python execution for every numerical task, require source citations on every claim, and use AI to eliminate the data-preparation layer entirely — so 100% of their billable hours go toward strategic advisory that clients cannot get from a spreadsheet.

The most profitable financial analysts in 2026 do not charge for data entry. They use AI to instantly structure and analyze raw data so they can dedicate every billable hour to high-level strategic insight. The stack costs $0–$40/month. The recovered billing capacity at 8 hours per week is $3,200/month at $100/hour. That arithmetic is available to every analyst reading this guide today.

The Verdict: Automate the ledger. Sell the insight. The analysts who master the Python-execution constraint and the citation requirement will produce financial deliverables that are faster, more accurate, and more defensible than anything produced manually — at a fraction of the time cost.

While you optimize your financial analysis stack, don’t leave opportunities on the table. Head to the SRG Job Board at /jobs/ for high-paying remote consulting contracts that respect your efficiency. Browse the SRG Software Directory at /software/ for detailed, verified reviews of the exact tools we use.

Take Smart Remote Gigs With You

Official App & CommunityGet daily remote job alerts, exclusive AI tool reviews, and premium freelance templates delivered straight to your phone. Join our growing community of modern digital nomads.